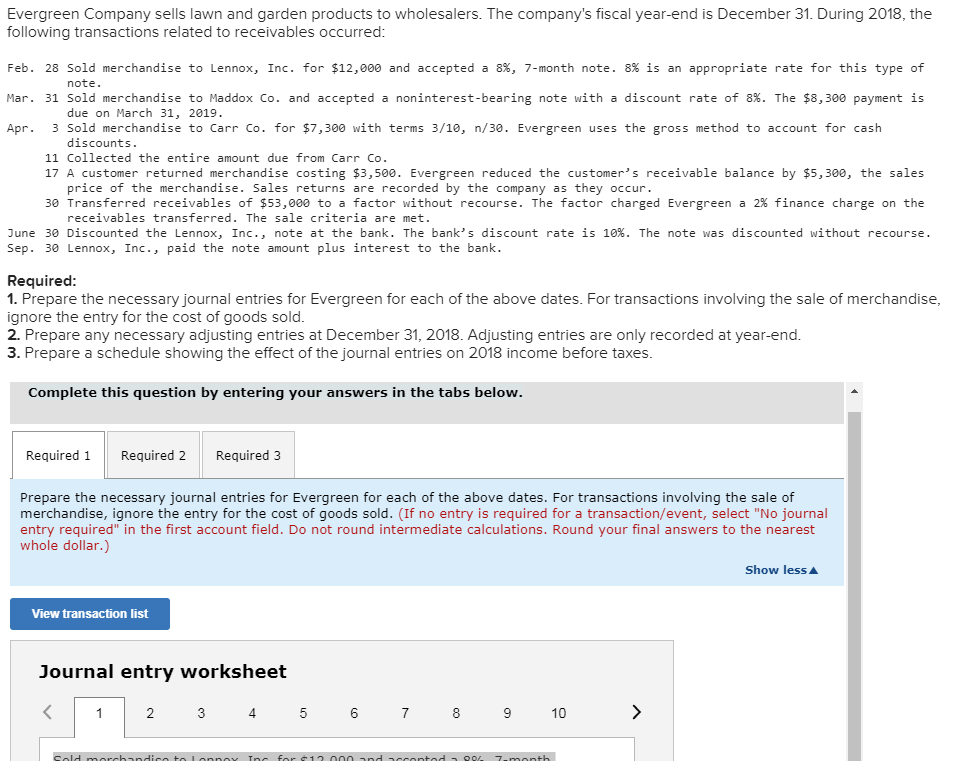

A home security mortgage is actually good “2nd financial”, a lump sum paid off over a flat time frame, making use of the house because equity. The loan also offers guarantee to own a secured asset-recognized security approved from the lender and often income tax-allowable appeal toward debtor.

Interest levels into such as fund usually are varying in place of fixed, but below fundamental next mortgage loans or playing cards. Financing terms usually are faster than earliest mortgage loans.

Home guarantee credit line

Property equity credit line (HELOC) is far more such as credit cards that utilizes your house because collateral. A maximum financing harmony is created, and citizen get mark with it during the discretion. Interest is predetermined and you may varying, and usually predicated on prevalent prime pricing.

After discover a balance due, this new citizen can decide the latest cost plan for as long as minimum attention payments are designed month-to-month. The expression from a HELOC last from around below five in order to more two decades, at the conclusion of which all stability have to be paid-in full. The attention might be tax-deductible, so it is more desirable than some alternatives.

Government benefit apps

Of a lot users given a reverse home loan might not see he’s eligible for authorities work with programs. You to definitely opposite mortgage guidance institution profile selecting most other alternatives to have 50% of one’s potential consumers they counsels. Offered experts are federal applications for example Supplemental Protection Earnings (SSI) and county and regional software particularly domestic time advice.

Fees and Authorities Recommendations

Opposite mortgages have been ideal just as one unit to lessen income taxes in senior years (Select Public Shelter taxation feeling calculator). Essentially, money from an other financial is not taxable and does not apply at Social Shelter or Medicare masters. Eligibility certainly bodies assistance programs is generally restricted.

“A face-to-face financial cannot connect with regular Public Shelter otherwise Medicare benefits. Yet not, if you’re on Medicaid or Supplemental Safeguards Earnings (SSI), any reverse mortgage proceeds you will get must be used instantly. Money you hold amount as a valuable asset that can perception eligibility. Such as, for people who located $cuatro,000 when you look at the a lump sum having household solutions and purchase it all the same thirty day period, everything is great. Any residual fund staying in your money next month do number given that an asset. In case your overall liquids tips (along with most other financial funds and savings bonds) go beyond $2,000 for someone otherwise $step 3,000 for some, you’ll be ineligible to own Medicaid. To-be secure, you really need to contact neighborhood Town Company into Aging otherwise good Medicaid expert.” (stress additional)

Contrary mortgages are extremely an increasingly popular option for the elderly just who must complement their senior years money, pay money for unforeseen scientific expenses, otherwise build expected solutions to their homes. Before entering into an opposite mortgage, but not, you’ll know what an opposite mortgage is, comprehend the type of contrary mortgages that are offered, understand the can cost you and you can fees associated with the opposite mortgages, and you can understand the installment financial obligation of these mortgages.

What’s a contrary Mortgage?

Reverse mortgage loans make it property owners to convert collateral in their home towards cash, when you find yourself sustaining possession. Collateral ‘s the difference between new ount loans Gulf Stream you owe on your home loan. The reverse mortgage will get their label once the as opposed to and come up with month-to-month mortgage payments on bank, you will get costs from your lender. As your bank makes costs to you personally, the total amount your debt toward loan expands plus collateral minimizes.

Although you aren’t guilty of while making monthly obligations towards the financing, because you will still be the master of the house, you still be the cause of spending possessions taxation, keeping home insurance, and you will and also make expected solutions.